Media Summary: In this Video we willl understand all the key concepts about Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into ES is a complement to value at risk (VaR). ES is the average loss in the tail; i.e., the

Expected Shortfall Explained With Excel - Detailed Analysis & Overview

In this Video we willl understand all the key concepts about Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into ES is a complement to value at risk (VaR). ES is the average loss in the tail; i.e., the Hello Candidates, In this video we will be talking about the concept of How to address the limitations of value-at-risk? One of the most famous techniques used to measure Designed for CFA and FRM Part 1 candidates, this video clearly and simply explains the Risk Management concepts of Value at ...

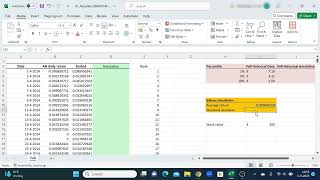

In this video, I'm going to show you exactly how we calculate In this video we discuss the limitations of VAR and how to overcome some of those limitations using Thanks for watching this video. As promised, here's the formula to compute the ES with the simulation approach: =(-SUMIF(BEGIN ... In my previous video, I showed you how we retrieve During the financial crisis of 2008, one particular measure of risk became very popular. Many financiers and government officials ...