Media Summary: Ever wondered what Value at Risk (VaR) or Designed for CFA and FRM Part 1 candidates, this video clearly and simply explains the Hello Candidates, In this video we will be talking about the concept of

Conditional Value At Risk Expected - Detailed Analysis & Overview

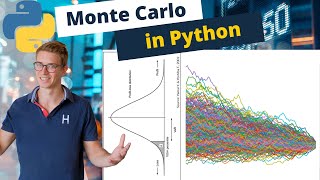

Ever wondered what Value at Risk (VaR) or Designed for CFA and FRM Part 1 candidates, this video clearly and simply explains the Hello Candidates, In this video we will be talking about the concept of In today's video we follow on from the Monte Carlo Simulation of a Stock Portfolio in Python and calculate the Implementation of Historical Value at Risk (VaR) and