Media Summary: Unlock the secrets of financial risk management with Ryan O'Connell, CFA, Hello Candidates, In this video we will be talking about the concept of In this video, I'm going to show you exactly how we calculate

Frm Expected Shortfall Es - Detailed Analysis & Overview

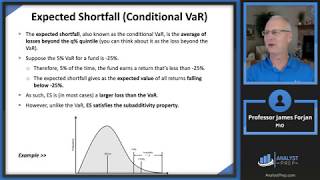

Unlock the secrets of financial risk management with Ryan O'Connell, CFA, Hello Candidates, In this video we will be talking about the concept of In this video, I'm going to show you exactly how we calculate ... via historical simulation and parametric approaches using normal and lognormal assumptions, Dive into the world of financial risk management with this comprehensive guide to Value at Risk (VaR). Ryan O'Connell, CFA, ... After completing this reading, you should be able to: ✓Explain the distinctions between economic capital and regulatory capital ...