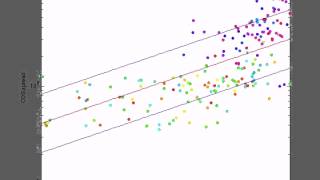

Media Summary: About ModelRisk: ModelRisk is the pre-eminent risk analysis tool for business, science, engineering and government. ModelRisk ... NOTE: CDS that fall below the lower error band will be shorted, and those that end up above the upper error band will be bought. What happens when you combine quantum machine learning,

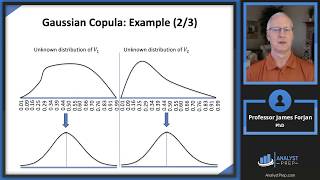

Credit Var Using Copula Simulation - Detailed Analysis & Overview

About ModelRisk: ModelRisk is the pre-eminent risk analysis tool for business, science, engineering and government. ModelRisk ... NOTE: CDS that fall below the lower error band will be shorted, and those that end up above the upper error band will be bought. What happens when you combine quantum machine learning, FRM Part 2 training for Equity Investments at PACE, Downloadable recorded videos for CFA, FRM trainings and skill based ... Here we are trying to estimate the value at risk for a bank's This educational video is part of the course An Introduction to

This book is essential for anyone involved in the intricate world of financial derivatives, risk management, and