Media Summary: The Gaussian copula was gainfully employed prior to the credit crisis, and it has pretty much been shamed. Mathematically, it's an ... This video is just one of many in a paid Udemy Course. To see the rest, visit this link: ... In this video, we break down the Gaussian Copula step by step using simple intuition and easy examples. You'll understand how ...

Financial Correlation Modeling Bottom Up - Detailed Analysis & Overview

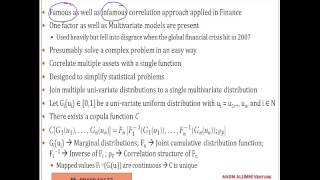

The Gaussian copula was gainfully employed prior to the credit crisis, and it has pretty much been shamed. Mathematically, it's an ... This video is just one of many in a paid Udemy Course. To see the rest, visit this link: ... In this video, we break down the Gaussian Copula step by step using simple intuition and easy examples. You'll understand how ... Describe the bivariate normal distribution. Play with the Fréchet-Hoeffding bounds: Outline: * Animation: Misconception about ... Method B, an alternative method for creating a multivariate distribution with metalogs, uses copulas with metalog marginal ...

Calculate covariance using the EWMA and GARCH(1,1) models. About ModelRisk: ModelRisk is the pre-eminent risk analysis tool for business, science, engineering and government. ModelRisk ...