Media Summary: Madeleine Udell, Cornell University Mini-symposium on Low-Rank Models and Applications ... This video is just one of many in a paid Udemy Course. To see the rest, visit this link: ... This lesson demystifies the bottom-up approach

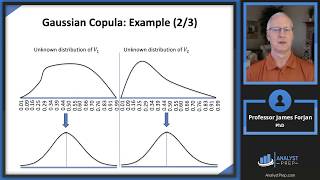

Var Using Gaussian Copula - Detailed Analysis & Overview

Madeleine Udell, Cornell University Mini-symposium on Low-Rank Models and Applications ... This video is just one of many in a paid Udemy Course. To see the rest, visit this link: ... This lesson demystifies the bottom-up approach I am Dr Krzysztof Ozimek, and my PDF textbooks and courses are science-based and draw on over 30 years of experience ... Dr Pavel Krupskiy (University of Melbourne) presents “Conditional