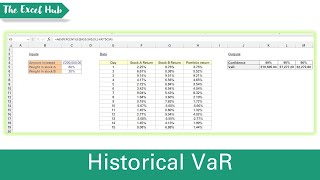

Media Summary: Risk Disclosure: Futures and forex trading contains substantial risk and is not for every investor. An investor could potentially lose ... Ryan O'Connell, CFA, FRM walks through an example of how to calculate Dive into the world of financial risk management with this comprehensive

Tutorial 10 Standard Historical Var - Detailed Analysis & Overview

Risk Disclosure: Futures and forex trading contains substantial risk and is not for every investor. An investor could potentially lose ... Ryan O'Connell, CFA, FRM walks through an example of how to calculate Dive into the world of financial risk management with this comprehensive The key learning outcomes for this episode are: 1) Introduction to Historical simulation and model building in estimation of Value at Risk (VaR) Today we are revisiting the application of basic

This video is taken from by basic RM course and deals with MR under the model-building approach.