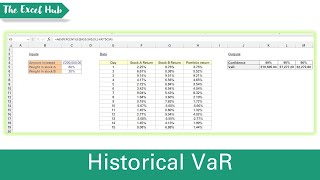

Media Summary: Ryan O'Connell, CFA, FRM walks through an example of how to calculate Dive into the world of risk management with this concise explanation of Dive into the world of financial risk management with this comprehensive guide to

Historical Method Value At Risk - Detailed Analysis & Overview

Ryan O'Connell, CFA, FRM walks through an example of how to calculate Dive into the world of risk management with this concise explanation of Dive into the world of financial risk management with this comprehensive guide to