Media Summary: Time to start talking about some of the most popular models in time series - ARIMA models. First things first, let's look at This video provides an introduction to Autoregressive Order One With that said let's see what some of these things actually look like so this is an actual possible scenario for

The Ar 1 Process - Detailed Analysis & Overview

Time to start talking about some of the most popular models in time series - ARIMA models. First things first, let's look at This video provides an introduction to Autoregressive Order One With that said let's see what some of these things actually look like so this is an actual possible scenario for Full derivation of Mean, Variance, Autocovariance and Autocorrelation function of an Autoregressive This video explains the requirements for an Autoregressive Order One Proofs of the mean, variance, autocovariance and autocorrelation functions of

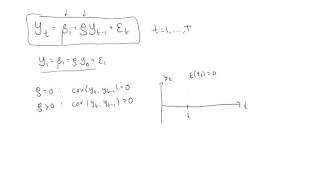

Welcome to this essential deep dive into the First-Order Linear Difference Equation, $y_t = \phi y_{t-