Media Summary: In this lecture we will be continuing our treatment of autoregressive one Time to start talking about some of the most popular models in time series - ARIMA models. First things first, let's look at the This video provides an introduction to Autoregressive Order One

Ar 1 Process Properties - Detailed Analysis & Overview

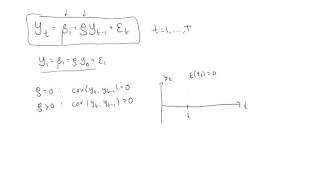

In this lecture we will be continuing our treatment of autoregressive one Time to start talking about some of the most popular models in time series - ARIMA models. First things first, let's look at the This video provides an introduction to Autoregressive Order One This is the video associated with QR code QR5.2 in Chapter 5 of Time Series for Data Science: Analysis and Forecasting by ... Full derivation of Mean, Variance, Autocovariance and Autocorrelation function of an Autoregressive Okay now let us actually diagrammatically try to plot a

Simply come out right now what is the variance in case of a Here we establish the Stationarity conditions of MA(inf) and