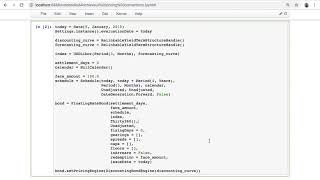

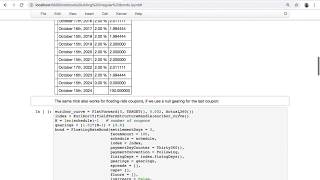

Media Summary: In this screencast, I show a caveat to keep in mind when performing In this screencast, I show how to build slightly more complex In this screencast, I describe a problem with using different day count

Quantlib Notebooks Mischievous Bond Conventions - Detailed Analysis & Overview

In this screencast, I show a caveat to keep in mind when performing In this screencast, I show how to build slightly more complex In this screencast, I describe a problem with using different day count Modeling a bond portfolio in modelx using QuantLib (no sound) QuantLib Integration: UK Gilts Pricing and Sensitivities The next parameter required is the date content the list is about the day counter