Media Summary: Derives formula for the price of a European call option under the Merton's BlackScholes Welcome to ! In this video, we ... BEM1105x Course Playlist - Produced in ...

Jump Diffusion Model In Python - Detailed Analysis & Overview

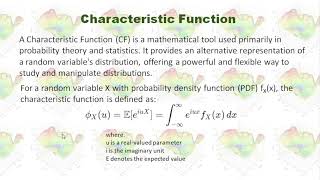

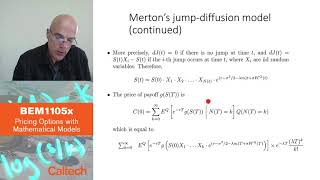

Derives formula for the price of a European call option under the Merton's BlackScholes Welcome to ! In this video, we ... BEM1105x Course Playlist - Produced in ... Learn about Monte Carlo simulation and how it is used in financial asset pricing Join this channel to get access to perks: Proudly sponsored by PyMC Labs: ... In this video, I will introduce the Merton