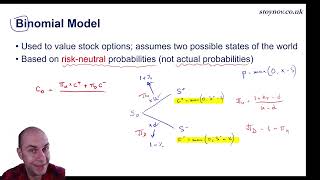

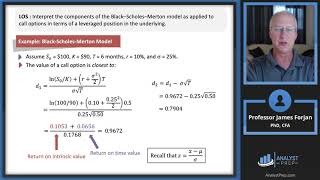

Media Summary: Smart hack to solve any problems related to The binomial model is a fundamental method for valuing This is an excerpt from our comprehensive animation library for

Cfa Level 2 Option Replication - Detailed Analysis & Overview

Smart hack to solve any problems related to The binomial model is a fundamental method for valuing This is an excerpt from our comprehensive animation library for Valuation of Contingent Claims Part II covers the Black Scholes Merton model and the