Media Summary: A backtest compares actual OBSERVED exceptions (aka, failures or exceedences) to EXPECTED; e.g., we observed losses in ... In this video, we will go through Crash Course Series - Chapter 4 - This is the first part of Lesson 6. Topics: -

Back Testing Var - Detailed Analysis & Overview

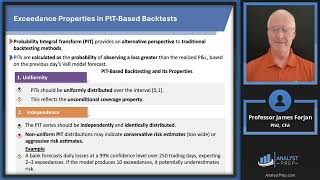

A backtest compares actual OBSERVED exceptions (aka, failures or exceedences) to EXPECTED; e.g., we observed losses in ... In this video, we will go through Crash Course Series - Chapter 4 - This is the first part of Lesson 6. Topics: - How one can evaluate whether a particular Kupiec (1995) unconditional coverage test (UCT) is one of the most famous Today we are applying an out-of-sample historical simulation